AI Versus Eroom's Law

Observations as an early-stage investor

Welcome to The Century of Biology! This newsletter explores data, companies, and ideas from the frontier of biology. You can subscribe for free to have the next post delivered to your inbox:

It’s been a busy quarter since I wrote about Sid’s incredible journey to cure his own cancer. This story has gone completely viral and driven an overwhelming amount of interest from patients, regulators, scientists, and founders. How can we scale what Sid has accomplished?

My wife and I also welcomed Rosalind to our family. Amplify Bio has been growing, too. Exciting times all around. You can check out a short essay I wrote about our investment in Infinitopes, an Oxford spinout working to develop the next generation of breakthrough cancer vaccines.

Today, we’re going to explore the case for optimism about AI-powered drug discovery.

Enjoy! 🧬

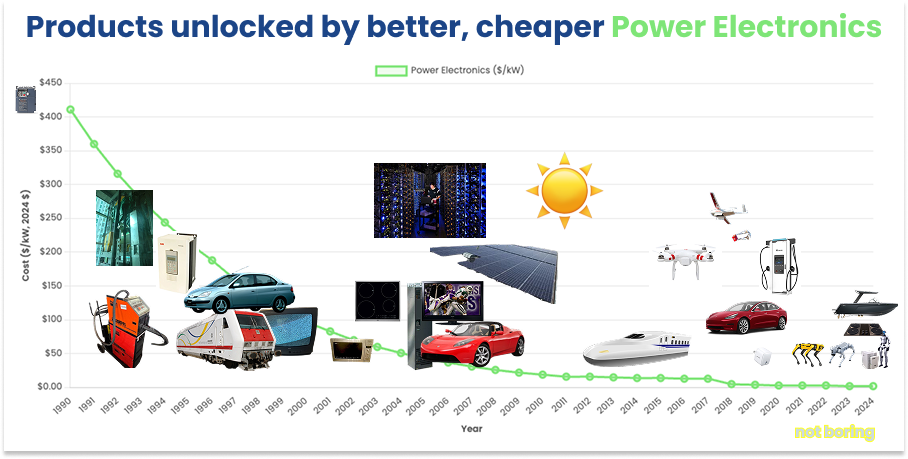

Typically, a steep cost decline for a foundational technology leads to a Cambrian explosion of new applications and products.

Moore’s Law gave rise to personal computers, portable computers, smart phones, smart watches, and even more questionable devices like smart fridges.

Packy McCormick recently analyzed in exhaustive detail how plummeting costs in the “electric stack” (batteries, magnets, power electronics, etc.) led to a similar proliferation of new engineering marvels.

This pattern hasn’t held for biomedicine. DNA sequencing has decreased exponentially in cost, alongside a whole slew of rapidly improving drug discovery technologies and therapeutic modalities. Despite that, there hasn’t been a meaningful increase in the number of new drugs approved each year, which hovers around ~50.1

And the cost to bring a new drug to market keeps rising. In fact, exponentially so.

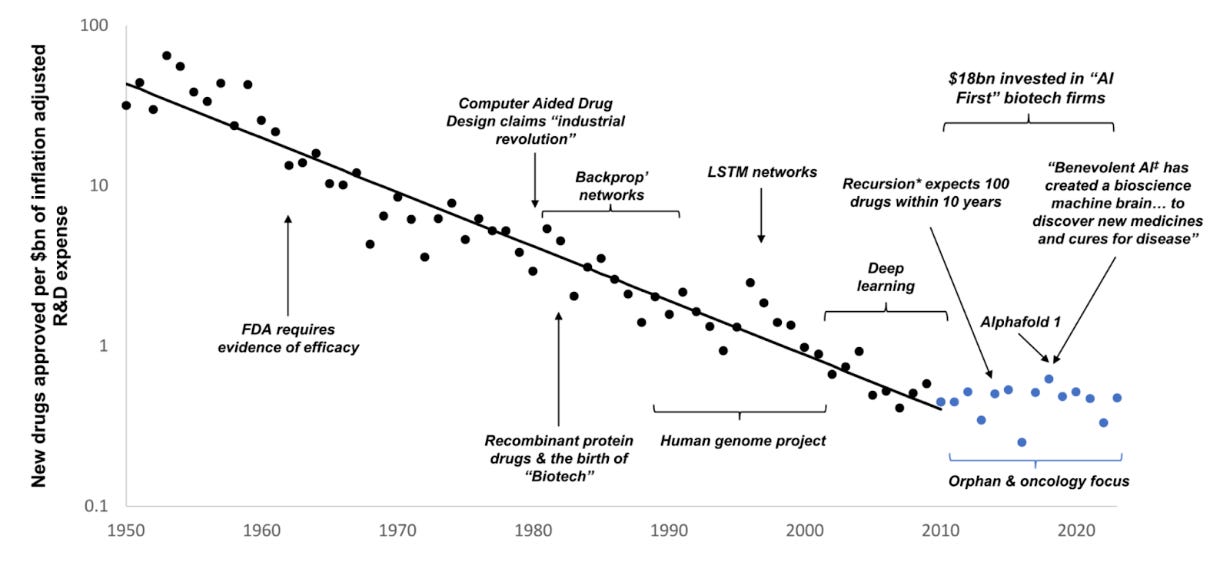

In 2012, an equity analyst named Jack Scannell and his colleagues published an article showing that “the number of new drugs approved per billion US dollars spent on R&D has halved roughly every 9 years since 1950.”

Recently, Scannell showed how this phenomenon, coined “Eroom’s Law” (the inverse of Moore’s Law), has steadily continued even with the birth of biotech, the Human Genome Project, and the rise of AI drug discovery.

Based on these observations, Scannell and others have voiced skepticism about expecting any different for the next wave of AI breakthroughs in the life sciences. Every time somebody posts a hyperbolic message about AI revolutionizing pharma, Scannell quips, “At last I understand why it costs 100x more to discover a drug today than in 1950. Our computers have slowed down.” (Other good ones here and here.)

Recently, Ruxandra Teslo, a fellow geneticist and writer, has published several great articles outlining why the cost of clinical development—not pre-clinical drug discovery—is the major driver of Eroom’s Law. And she has detailed why policy rather than technology is likely the biggest lever to solve this problem.

Teslo is now a Fellow at Renaissance Philanthropy working to make her vision for Clinical Trial Abundance a reality. Her research here is excellent, and if you haven’t checked out her personal newsletter yet, you should.

Several founders have made the bet that technology can meaningfully reduce the time and cost of trials. I’ve written about how Vial aims to do this. Similarly, Formation Bio is focused on developing their own AI-powered clinical infrastructure.

When explaining the rationale for this focus, Ben Liu, the CEO of Formation, outlines a similar view that discovery is no longer the bottleneck. He tells a story of pitching an exciting academic drug candidate to pharma, only to be told, “We already have more good drugs discovered than we can afford to prosecute.” He goes on to say that “if there’s one competitive advantage that you want to have as a pharma company, ironically it isn’t in discovery. It’s actually in the drug development process.”

I agree with a lot of this.

Scannell’s meta-analysis is foundational work. Teslo’s efforts on regulatory innovation and clinical trial abundance are sorely needed. Vial and Formation are tackling real problems and have the potential to be generational businesses.

The rising cost of clinical development is the primary driver of Eroom’s Law.

At the same time, I spend most of my efforts as an early-stage biotech investor on discovery, with a focus on new technologies and approaches. I still think this has the chance to deliver real impact and great returns.

I want to make the case for both points here.

I think that AI will help make more and better medicines.

I also think that there are a lot of misconceptions about biotech investing, especially in new platforms, let alone AI platforms. Similar to Bruce Booth’s classic “defense of life sciences investing,” I want to unpack why this is an attractive investment.

Here, I’ll outline three arguments:

Pharma R&D efficiency is not the same thing as biotech R&D efficiency.

Better trial regulation and infrastructure would be a big win for little biotech.

Discussions centered on efficiency may miss the point when it comes to AI-enabled drugs.

To start, let’s examine the nature of the relationship between biotech and pharma.

On the Financialization of Pharma

Many of the largest pharma companies have been around for a long time and have wacky origin stories. I previously wrote about how some of these 100+ year old businesses started out making dyestuffs for textiles before using their chemistry infrastructure to make pharmaceutical products. Obviously, these businesses have evolved considerably. And the world around them has, too.

Skipping over some very interesting history, some of the most critical business model evolution for the pharma industry started in the 1990s. Three major trends collided to restructure how drugs are discovered, developed, and sold.

The first trend was the increasing financialization of the global economy, especially in developed countries. This term has been defined in many ways, but the core idea is simple. As markets mature, there is a trend towards the finance industry accounting for a larger percentage of economic activity over time.

Consider the U.S. economy. From 1980 onwards, the share in GDP of the financial sector has roughly doubled on a percentage basis.

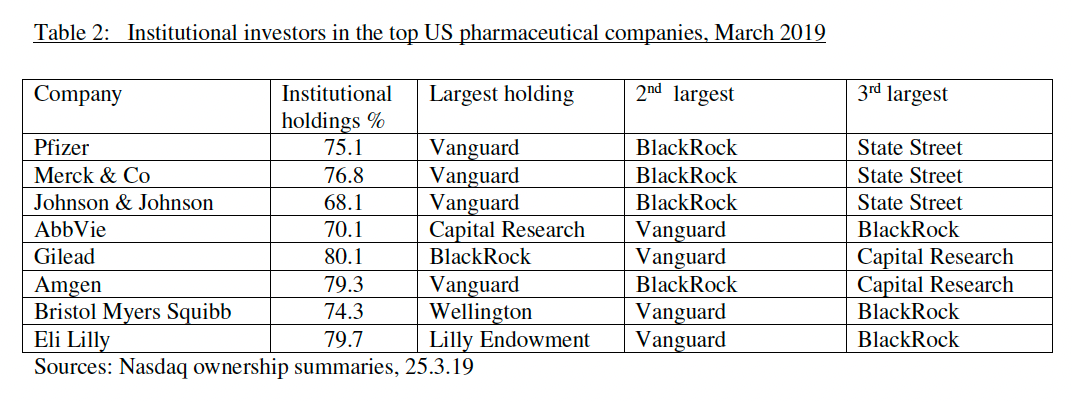

Investment products have increased in complexity and investment firms have scaled massively. Pharma has not been immune from this evolution. The shares of the largest pharma companies are now primarily owned by the world’s largest institutional investment firms.

This change in ownership was accompanied by different incentives. Pharma companies came under greater pressure to increase efficiency and maximize value for shareholders. As a result, these businesses began to spend much more of their earnings on dividends and share buybacks. The percentage of pharma executive compensation that comes in the form of share options and share awards is now also much higher than most other industries.

This trend is generally referred to as the financialization of the pharmaceutical industry.

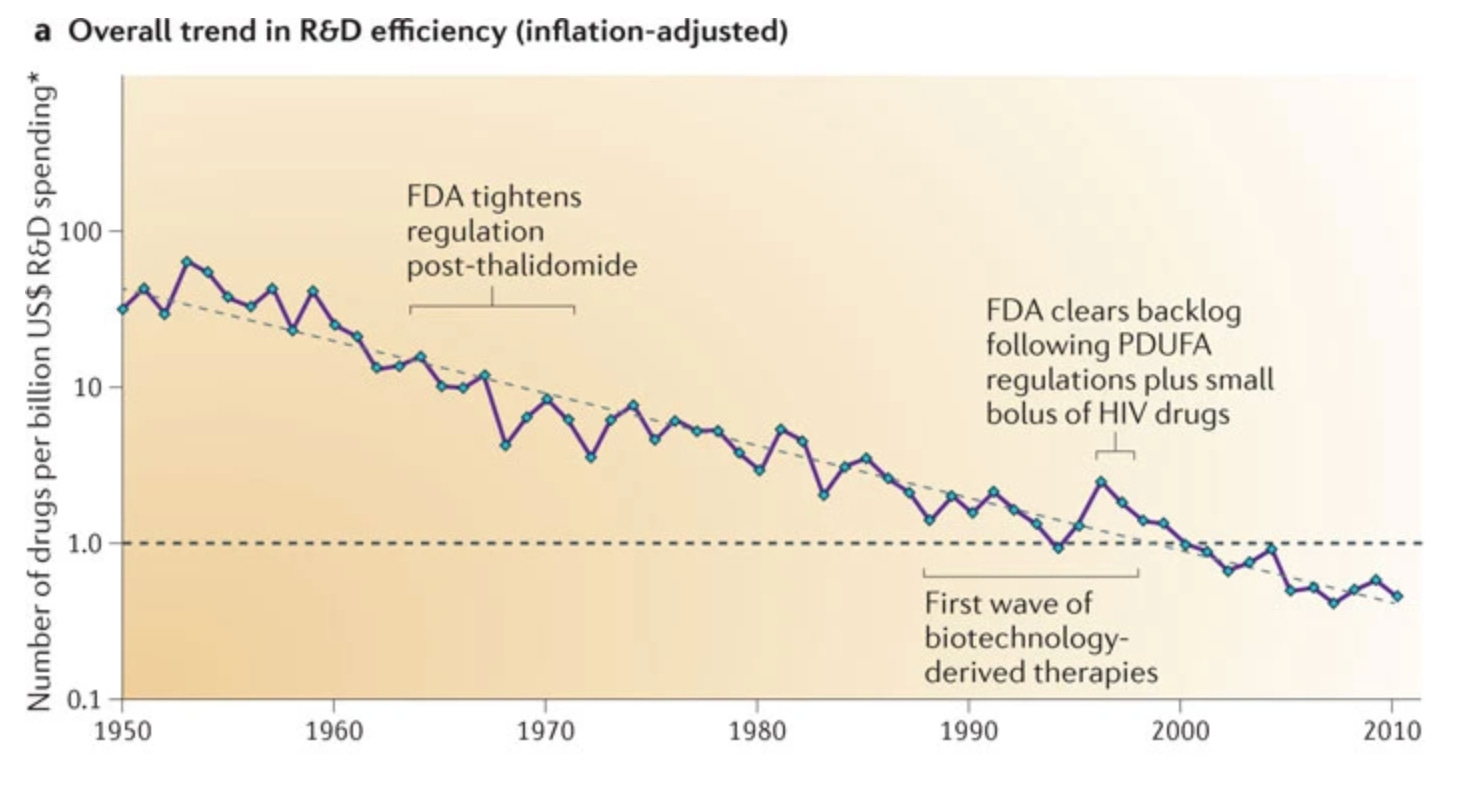

In parallel, the trend of exponentially declining R&D efficiency (since the 1950s!) showed no signs of slowing up. Pharma executives were forced to answer hard questions about what to do.

Faced with declining R&D efficiency, looming patent cliffs for some of the first blockbuster drugs, and shareholder demands for increased profits, several large pharma companies decided to consolidate.

Mergers combined revenue, cash, and resources. Circling the wagons, so to speak. Scale has advantages. But the decline in R&D efficiency didn’t stop. Another solution was needed.

This brings us to our third trend: the rise and maturation of the biotech industry. Breakthroughs in genetic engineering led to the first wave of biotechs such as Genentech, Biogen, and Amgen. These businesses focused exclusively on R&D. Their entire raison d'être was to bring a wholly new category of medicines to the market. By definition, these startups didn’t have the clinical infrastructure or commercial scale of big pharma.

A natural symbiotic relationship quickly emerged. Pharma companies began to hunt for innovation externally. And biotechs leaned into these partnerships for early financial stability and the existing channels to bring their products to market.

Over time, two important things happened. First, the aperture of biotech expanded far beyond recombinant DNA, encompassing a wide range of approaches to early-stage drug discovery. Second, pharma started divesting their own internal R&D and manufacturing efforts and focused more heavily on acquisition for new products.2

As one analyst wrote, “The large, complex organizations of the originators [pharma] are unsuited to fostering innovation. An ecosystem of venture capital has proven much more effective in selecting early-stage biomedical research opportunities. Essentially, venture capitalists today pre-finance the early-stage development for pharma companies.”

As my friend and fellow investor D.A. Wallach describes it, we are basically the “crazy guys” that stepped in to underwrite early-stage drug discovery risk. When stuff works, pharma can just buy it, rather than wasting a lot of money on R&D themselves.3

It’s worth underscoring how big this trend is. At this point, roughly two out of three Phase 1 trial submissions come from “emerging biopharma” companies with less than $200M in R&D expenditures and annual sales of less than $500M.

In her research on this topic, Joanna Shepherd, a legal scholar at Emory, wrote, “Whereas a few decades ago almost all drug discovery took place inside traditional pharmaceutical companies, today most drug innovation is externally-sourced from biotech companies and smaller firms. Internal R&D is no longer the primary source, or even an important source, of drug innovation.”

So, let’s consider the following take:

Pharma may have historical backlogs of molecules, but they are absolutely hungry for promising new experimental medicines. Over $1 trillion dollars have gone towards pharma M&A since 2010. This is how biotech works.

With this structure in mind, let’s turn our attention to the cost of drug development.

It turns out that modeling the cost of R&D is a contentious topic with estimates that vary wildly, ranging from $161 million to $4.54 billion per approved drug. The reason for the huge spread is that people don’t agree on what costs should be included. Methodologies are varied.4

A recent research report on this topic broke down the three components of R&D cost for a new medicine that makes it to market:

Out-of-pocket (OOP) costs of R&D incurred year by year.

The cost of capital combined with the number of years it takes to bring

a new medicine from discovery to being sold on the market for use with

patients.

The attrition rate, i.e. the percentage of successful medicines relative to

the number researched at the outset.

When people say things like, “It only costs ~$200M to get a drug approved,” this is likely a claim about the OOP costs. When people say things like, “It costs ~$4B to get a drug approved,” this is likely a claim about R&D costs, plus the opportunity cost of not investing the money elsewhere, multiplied by an assumed clinical probability of success.5

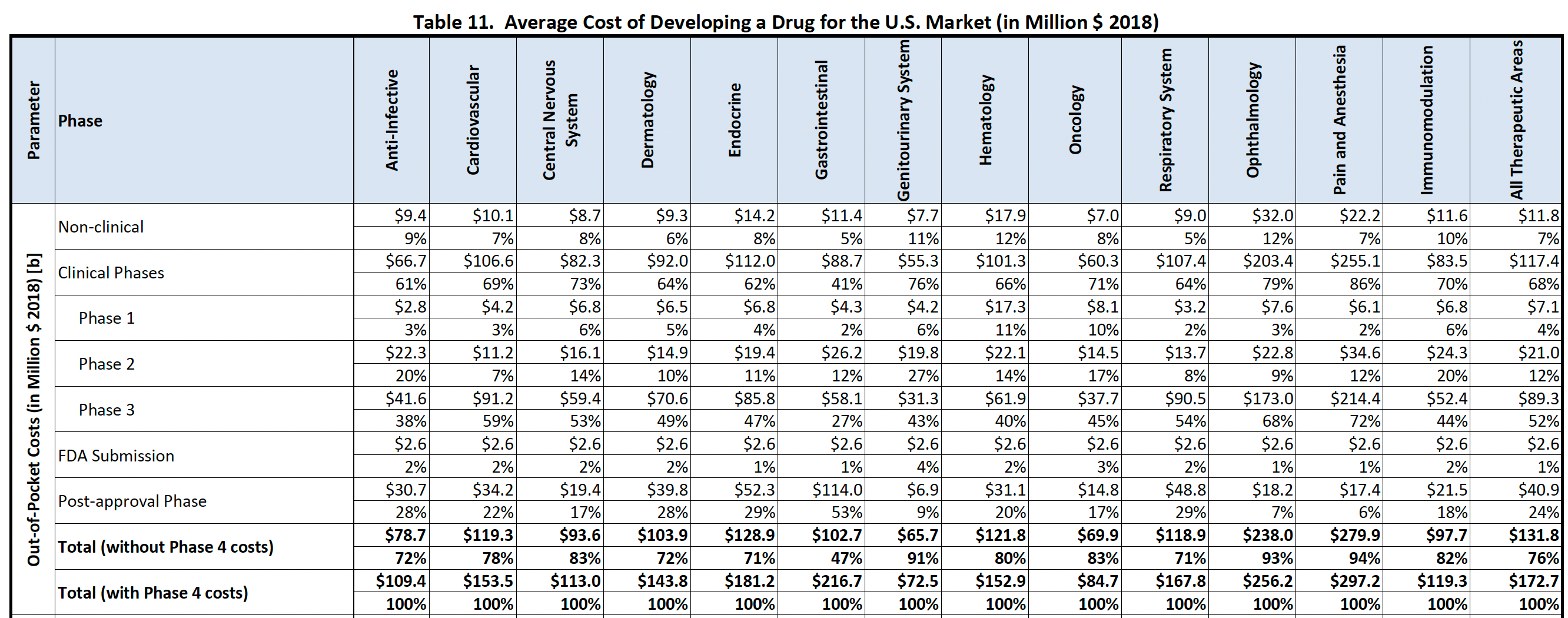

For simplicity, let’s focus on OOP costs. We’ll consider the numbers from a report prepared for the HHS in 2024:

Focusing on the numbers across all therapeutic areas, non-clinical R&D was estimated to account for only 7% of spend. The authors of the report wrote, “The clinical phases of drug development (Phase 1, 2, and 3) are the largest contributor to total out of pocket development costs, comprising around 68 percent of total costs inclusive of post-approval studies.”

Looking at this picture, discovery looks like a drop in the bucket. One could even argue it makes more sense to invest in reducing the cost of post-approval studies, which cost more than three times that of non-clinical R&D!6

But in reality, that’s not quite how things work.

As we just outlined, there are normally two parties that split these R&D costs:

The small biotechs that fund discovery and early-stage proof-of-concept, and

The big pharma companies that buy assets (or partner) and fund late-stage development and post-approval studies.

Considering this fact, the relative percentages for a small biotech are quite different. The ~$90M for a phase 3 study (let alone multiple phase 3 studies) and the ~$40M for post-approval studies are often not their problem. On a relative basis, the cost of non-clinical development is actually a bottleneck.

The discovery phase can cost more than the first trial. In aggregate, non-clinical costs are ~30% of the total spend through Phase 2, which is typically the steepest point of value inflection and de-risking. And critically, the discovery phase is what dictates whether or not there will be any return at all! The quality of the science and the molecule determines whether or not anybody will show up to fund the proof-of-concept study.

And this ignores one of the most costly factors of all: time! When tackling exceptionally difficult problems, discovery campaigns can drag on for years, consuming more resources than early clinical studies. Numbers can soar past the $11.8M estimate for non-clinical work.7

Which means that more efficient discovery can have a big impact on biotech returns!

Biotech R&D efficiency and pharma R&D efficiency are not the same thing. To Ben’s point, development efficiency is a great competitive advantage for a pharma. For a biotech, the name of the game is efficient and differentiated discovery.

Remember, we are the “crazy guys” doing the discovery work that pharma largely divested! But the definition of insanity is doing the same thing over and over and expecting different results. If we can find new ways to attack this problem and more reliably generate value, it is a very attractive opportunity.

Thankfully, there are many examples of greatly improved biotech efficiency even while the macro trend of Eroom’s Law has continued.

One example is the use of human genetic evidence to develop drugs with much higher success rates. Drug mechanisms supported by genetic data are ~2-3x more likely to succeed. This is a clear example where a new measurement technology can greatly improve R&D success rates.

BridgeBio, a hub-and-spoke biotech that is exclusively focused on this opportunity set, has success rates far higher than industry averages.

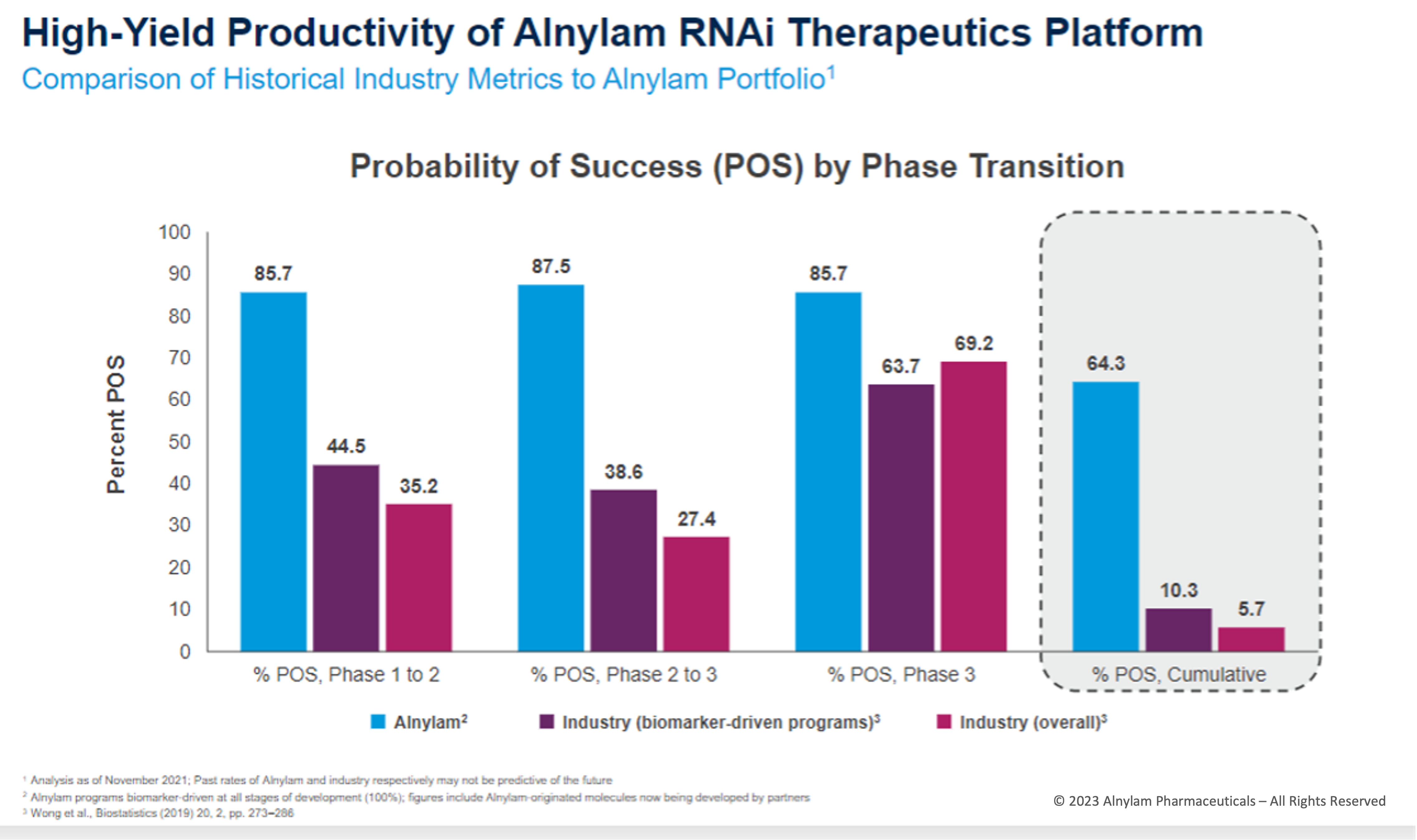

It’s also possible to invent new drug modalities that have a higher clinical success rate. Alnylam is a canonical example. Their RNAi platform makes it possible to drug genetically validated targets with astonishing accuracy.8

In aggregate, biologics have consistently been estimated to have roughly double the success rate of small molecule drugs. If we think back to the three factors of R&D costs, halving attrition rates in our industry should make a dent on the economics of our industry in the long run.

New technologies can and do make an impact on R&D productivity.

This picture leads to a slightly more hopeful mindset when it comes to AI for drug discovery. Rather than assuming all prior R&D innovation has been for naught, the question becomes: can AI have as big of an impact as human genetics or biologics?

“AI for drug discovery” is a broad enough term to encompass many things. There are many efforts to use AI for both target discovery and drug design—across basically every drug modality you can imagine. And new ideas are constantly being tried.

Some of the first movers, like Recursion Pharmaceuticals and Insilico Medicine, emphasized the use of robotics, large-scale data capture, and compute to systematize drug discovery. These businesses moved the industry forward and are advancing internal pipelines of new medicines.

The subsequent generation of founders learned from the first wave and put forward new ideas.

Consider Viswa Colluru and Ron Alfa, two members of the “excursion” mafia. Viswa founded Enveda, which uses AI to explore the chemical space produced by living systems (natural products). In only seven years, Enveda has raced into the clinic with a large pipeline of new molecules, several of which are already showing strong results. Ron founded Noetik, which uses AI to get as much information as possible from valuable primary human tissue samples.

Both ideas are centered around acquiring the data that will deliver the most predictive validity for new AI models. Already, self-reported “AI biotechs” are proving they can make drugs faster and with greater clinical success. With each iteration, founders are testing new theses about what will drive the greatest improvement on both fronts.

Again, this will not be the biggest driver of cost reduction in late-stage clinical development. We should expect to see the impact first show up in improved returns for biotech investment, rather than the fully loaded costs for a big pharma company to get a new drug approved.

Let’s assume this happens. Biotech investment becomes much more attractive. More exciting new drugs make it through proof of concept faster.

Will we still be rate-limited by the number of drugs that big pharma can ingest? In theory, yes. Which is why little biotech may benefit the most from regulatory innovation for clinical development.

Building to Endure, Not to Sell

Let’s recap. Most early-stage innovation comes from biotechs. But the primary exit strategy for biotechs is to sell to pharma, rather than to incur the costs of late-stage development and commercialization themselves.

This is arguably a good setup for both parties. Biotechs can have a laser focus on R&D. And there are less duplicative efforts to build massive sales forces for every company. Pharma can amortize these costs, putting “multiple products in the bag of sales reps” in a way that single-product drug companies cannot.

But there are consequences. One major issue is that the preferences and risk tolerance of big pharma can bound the set of ideas that biotech companies pursue. In other words, taste can be top down rather than bottom up.

Consider the case of GLP-1 drugs. Over the last few decades, biotechs have increasingly crowded their efforts around the targets that have been de-risked and prioritized by pharma. Ultimately, it was two pharma companies, Eli Lilly and Novo Nordisk, that pushed forward the original breakthrough products in obesity and weight loss.

David Yang wrote a great post about this dynamic, saying, “Investors rely heavily on pharma for exits, and there was little pharma M&A interest in obesity.” Once the first big products validated the market opportunity, early-stage investors financed the companies making the next generation of drugs in this space. We’ve already seen a string of big acquisitions rewarding this activity.

Relying on pharma as top-down tastemakers can stifle the emergence of new therapeutic ideas from startups.

This is not a minor issue. Biotech founders and investors overlooked the biggest product opportunity in the history of our industry because of this bias!

But there is also just a simpler numerical problem: there is a finite set of companies with the scale to consistently pursue late-stage clinical development. Each company can pursue a finite number of new products.

If this doesn’t change, why should we expect an increase in new drug approvals per year?

So let’s run a thought experiment.

We wave a wand. Poof! Clinical trials cost 10x less. Swish! Hundreds of new surrogate endpoints suddenly make many trials 5x faster. Pow! The cost and time to file a biologics license application (BLA) or new drug application (NDA) with the FDA goes from ~$4.68M and ~1-1.5 years to ~$300k and ~3 months.9

One possible outcome is that pharma companies could acquire and commercialize more drugs for the same total cost.

Another possible outcome—which I find quite exciting—is that we could see the birth of a new generation of enduring biotechs commercializing their own products. If it becomes more financially viable to launch your own product, why sell?

George Yancopoulos, the co-founder and CSO of Regeneron, has spoken openly about the dramatic increase in trial costs since the company’s inception. Founded in 1988, Regeneron is one of the rare biotechs to scale from a startup into a $100B+ company. In an interview with Matt Herper of STAT News, he said that it cost $10,000 per patient to conduct a clinical trial when the business first started. Now, it can cost as much as $500,000.

With this increase in costs, would it be possible to build Regeneron again in 2026?

In the conditions of our thought experiment, it would be much more likely.10

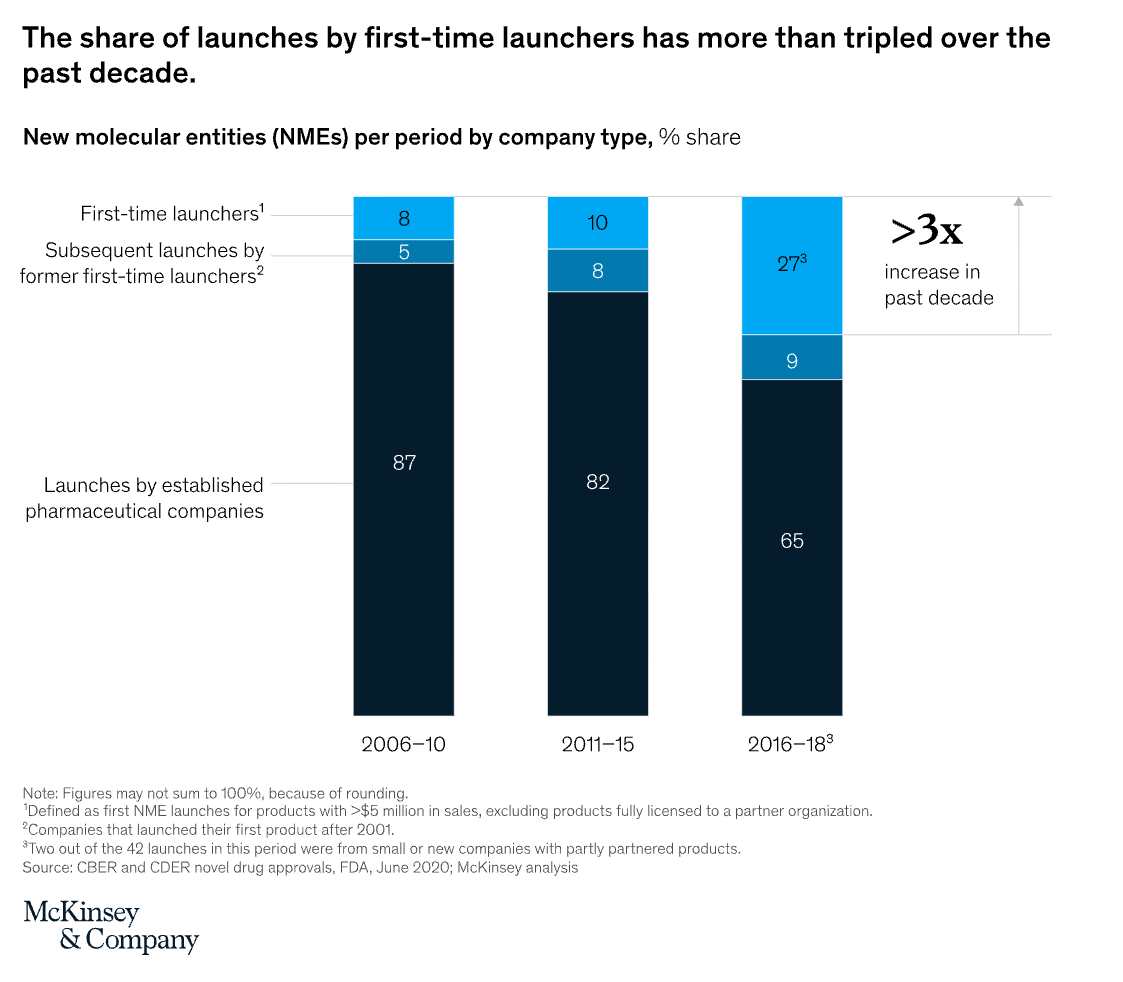

Recently, we have seen an uptick in the number of “first-time launchers” making the transition from R&D organization to commercial enterprise.

But this growth has primarily been a function of greater capital availability, not greater capital efficiency. In the last market cycle, low interest rates and strong pharma M&A activity drove more dollars into biotech. Valuations increased. At a certain point, the price pharma would pay was lower than what investors would pay. So more companies decided to go it their own and become commercial organizations.

Now let’s imagine the capital efficiency scenario: companies are able to get to product approval faster and at much lower cost. This could drive a similar dynamic where biotechs can finance at more attractive terms than what pharma can afford to pay.

If we make trials faster and cheaper, could we see an even bigger wave of first-time launchers?

What if biotech efficiency (early-stage R&D) and pharma efficiency (clinical development and commercialization) both improve?

Hyper-efficient discovery firms are able to vertically integrate and become full-stack drug companies.

Could we go from ~50 drugs a year to ~500?

The points I’m making here are admittedly a bit nuanced.

I’m arguing:

Better discovery matters. The market financing early-stage discovery is its own little universe that is less directly impacted by Eroom’s Law.

If we can make clinical development more efficient, the biggest impact could be on the early-stage companies that would be able to swim out of their local estuaries and compete in the open sea with their own products, like Regeneron once did.11

If discovery becomes more efficient, more money should flow into biotech. If development becomes more efficient, more biotechs should become enduring, independent companies. These companies have the potential to get very big, further reinforcing the flywheel of more capital into biotech.

Patients would get more medicines, faster.

One way to talk about investments is to outline the “bear case,” the “base case,” and the “bull case” scenarios. The bear case for AI biotech is that it underperforms more traditional discovery approaches. The base case is that AI-enabled companies do at least as well as their traditional counterparts, and some do much better. The bull case is that a huge tailwind of regulatory innovation enables some of the most successful players to break out and become generational drug discovery companies.12

But the ultimate impact of AI on biomedicine may have nothing to do with efficiency.

Digital Biologics

My friend Simon Barnett, who runs research at Dimension, gets “annoyed at the concept of an AI drug.”

His point is valid. Our industry has developed a genuinely annoying habit of arguing about whether or not any “AI drugs” have been approved yet. Normally, people use this term to mean conventional drugs that have been developed using AI discovery tools. This opens the door to an elaborate semantic argument about which drugs do or don’t meet this bar. It isn’t very productive.

But there is a growing set of true AI drugs—those that consist of both algorithms and biology, bits and atoms. If Digital Biology is the discipline at the intersection of computation and the life sciences, let’s call this new category of products Digital Biologics.

Consider the following examples.

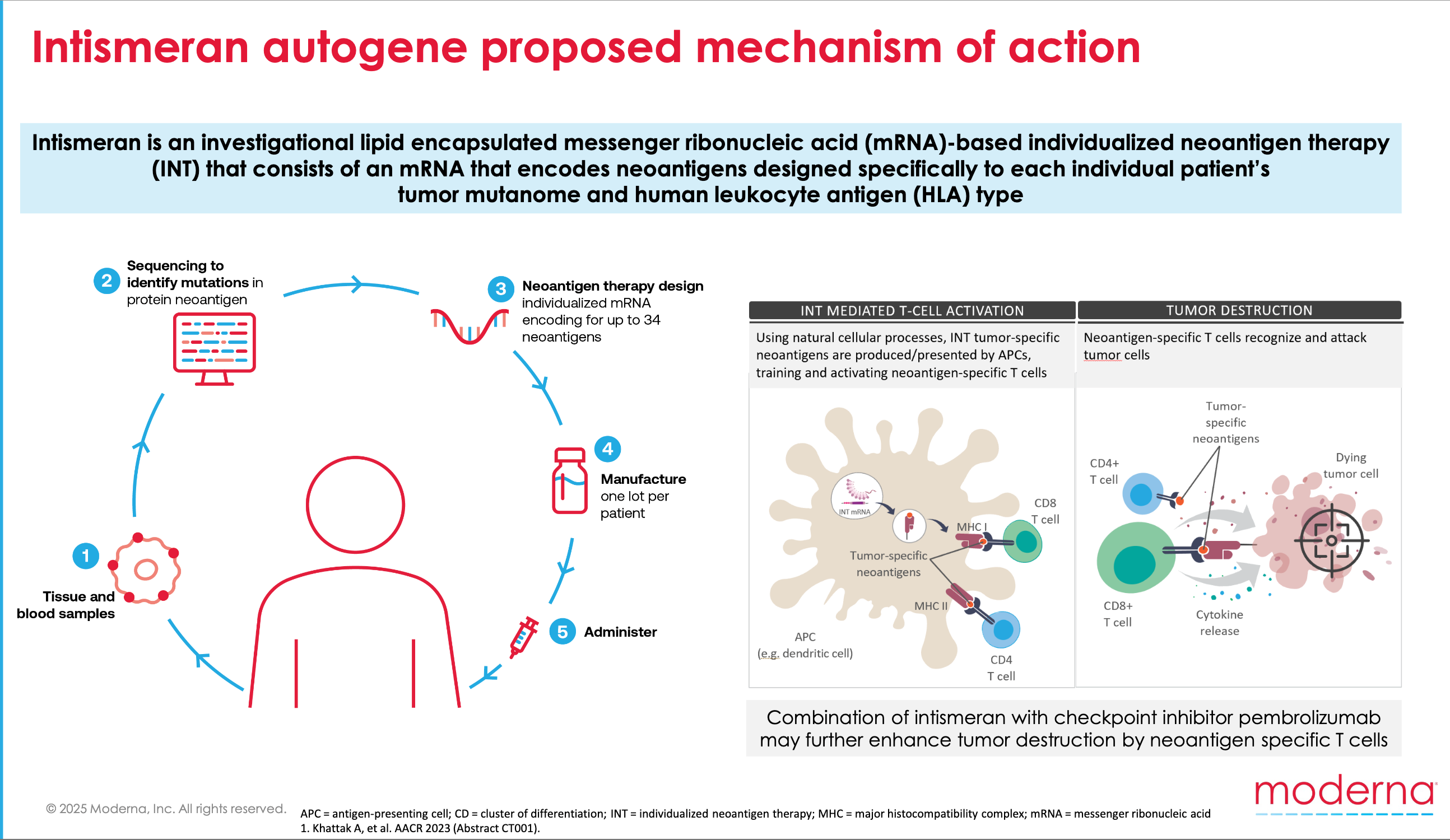

Moderna has developed a personalized mRNA cancer vaccine called intismeran autogene. Merck and Moderna partnered to test this vaccine in combination with Keytruda in clinical trials. So far, they’ve seen a 49% reduction in the risk of cancer recurrence or death after five years of follow-up in Melanoma patients.

How does the vaccine work?

First, a patient’s tumor is sequenced. Next, a machine learning algorithm sifts through the sequencing data and ranks the most likely cancer-specific antigens. Then, “Upon administration into the body, the algorithmically derived and RNA-encoded neoantigen sequences are endogenously translated and undergo natural cellular antigen processing and presentation, a key step in adaptive immunity.”

I don’t know about you, but that sentence gives me chills. Am I quoting a science fiction novel? Nope, a Merck press release. What a time to be alive.

What is the drug? The RNA molecules? But you don’t get those without the algorithm. So is it the algorithm? As I’ve argued, I think the answer is that it is both things. The drug is the composite process of computational design and molecular instantiation.

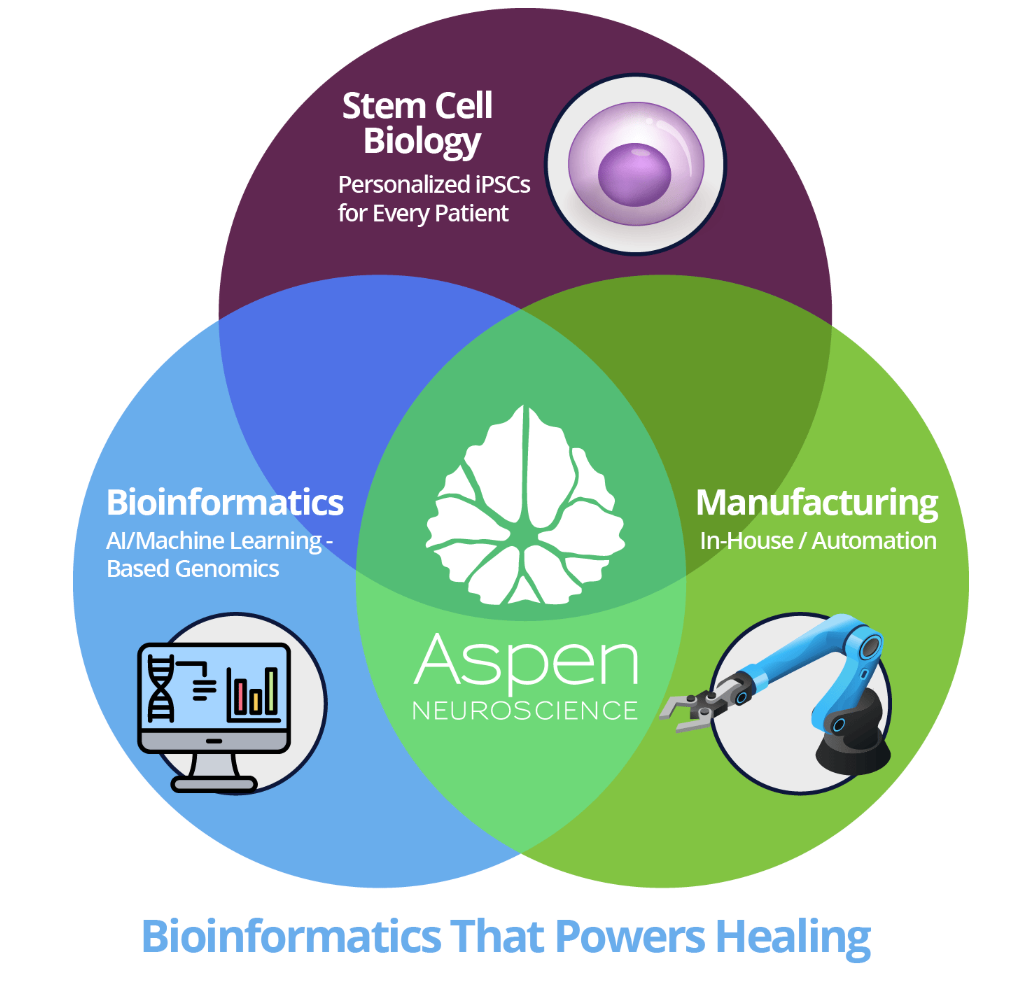

Another example is sasineprocel, a new cell therapy product for Parkinson’s disease being developed by Aspen Neuroscience. In a Phase 1/2a study, all eight patients treated with the experimental therapy showed improvement. Some responses were dramatic:

Videos of one patient, recorded before treatment and at the one-year mark, were particularly striking to the Aspen team. Before receiving sasineprocel, the patient struggled to stand from a chair, open a door and walk down the hallway, with a low voice and a muted facial expression, McDevitt said. One year after the treatment, he is “like a different person,” rising from the chair and walking straight out the door with a smooth gait.

“It’s night and day,” McDevitt said, with the video making many at the company emotional. “There were a lot of tears.”

Sasineprocel is a complex product that combines cutting-edge cell engineering and bioinformatics. The first step is to collect a small biopsy of the patient’s skin. The skin cells are then transformed into pluripotent stem cells (iPSCs), which are differentiated into dopaminergic neuronal pre-cursor cells (DANPCs). When injected, the aim is for the engineered cells to “restore dopamine function and rebuild neural networks.”

This intricate transformation process is carefully controlled by a suite of four machine learning algorithms powered by genomic data: PluriTest, NeuriTest, GraftTest, and DopaTest. Without a scalable and data-driven approach, it’s hard to imagine that this therapeutic strategy would be viable. As their Director of Bioinformatics said, these tools are “the final check point for making autologous cell replacement therapy a personalized medicine reality for people with Parkinson’s.”

Again, what is sasineprocel? It’s definitely not an invariant chemical structure with discrete IP. But is it just the neuronal pre-cursor cells that are administered? Or is it the composite process required to administer the cells, algorithms and all? It feels like the latter.

Intismeran and sasineprocel are both Digital Biologics. My prediction is that there will be more products like this over time, not less.

Other Digital Biologics may have a more distinct separation between platform and product. We may be able to front-load more of the AI to make off-the-shelf cancer vaccines. Exquisitely complex AI-designed cell therapies may be manufactured like other cell therapies.

But these drugs will start to feel like the “Move 37” moment where AlphaGo played a 1 in 10,000 move to pull ahead of the best human Go player. AI could help enable sophisticated multi-specific antibodies that were previously out of reach of even the best antibody engineers. The “AI drug” distinction will start to feel less arbitrary.

Bending the arc of Eroom’s Law is super important for our industry.

One of the most impactful levers of change is likely to be regulatory innovation. If America wants to remain competitive in clinical development, this is sorely needed. Hopefully it’s clear that I’m in complete agreement with the brilliant people working to make this happen.

My arguments here are threefold.

First, innovation in discovery is still critical. Biotech companies live and die by their ability to make breakthrough medicines. For the startups that deliver most of the new products in our industry, this is still a bigger bottleneck than the ballooning costs of late-stage clinical development.

Second, if we succeed in reducing trial costs, it could fundamentally alter the relationship between little biotechs and big pharma companies. We could see a new wave of full-stack drug companies like Regeneron. This could be how we see an order of magnitude more drugs get to market every year.

Third, efficiency is not the only story for AI drug discovery. Cancer patients are living longer and Parkinson’s patients are walking because of a new wave of Digital Biologics. These medicines aren’t exciting because of a quantitative shift in discovery timelines. They represent a qualitative shift in what is possible.

Faster and cheaper trials would enable more of this.

Should we focus on accelerating discovery or development?

The answer is yes.

There has been a modest upwards trend over time. The latest 5-year average for FDA approvals is 48. The average since 1993 is 36. That’s a 33% increase, but we haven’t gone from 36 approvals to 360 approvals.

This is another clear example where pharma efficiency ≠ biotech efficiency. When pharma companies deprioritized R&D, there was an exodus of highly skilled scientists. Many joined contract research organizations (CROs). One widely used analogy for CROs is that they are like AWS for biotech startups, because they can dramatically reduce what a company needs to build internally. A loss of talent and expertise for pharma, but a big win for biotech.

Conversations with D.A. greatly helped me first understand this industry history. Thank you!

Another challenge in accurately modeling drug R&D costs is that the most important data is proprietary within companies.

Sometimes the OOP costs for large indications—such as cardiovascular diseases—can climb into the billions. Big pivotal trials with a lot of patients are expensive, especially when done multiple times. The per-patient-costs in oncology trials are also higher, which is part of why new cancer drugs cost more than most other types of drugs.

This is a good idea. And it’s a problem that PicnicHealth, a company Amplify partnered with, aims to solve.

Of course, anything we can do to reduce the time and cost and cost of first-in-human studies also will be great for biotech efficiency. This is why startups often run clinical studies in Australia or China. FDA innovation to achieve parity is critical.

Regeneron is another example of a company with prolific R&D output. They also rely on human genetic evidence and biologics.

These numbers are intentionally provocative, except for the cost to file. That would simply match the costs of the EMA.

Remember, Ben’s point about building Formation is that “there hasn’t really been a big pharma company created since the 1980s” because of this increase in the cost of clinical development. He’s working to change that.

a16z has outlined The Little Tech Agenda, which is a policy stance focused on enabling tech startups rather than tech incumbents. Basically, my argument is that any major regulatory innovation for clinical development is The Little Biotech Agenda.

If the technology is good enough, some companies could even reach escape velocity without regulatory innovation. Business model innovation, such as hub-and-spoke strategies, may help, too.

Nice piece. My comment: not so much the cost per se (IMHO) but as you point out it's the massive %age of failures (>90%) even after drugs get to Phase 1 by when supposedly things are supposed to look rosy. The breakdown of failure is roughly 40% non-efficacious, 40% toxicity, 20% business reasons. THIS is what needs fixing, and until Pharma takes a SYSTEMS approach instead of doing molecular biology on supposed targets it will not get better. Successful drugs are successful because they hit multiple targets (see e.g. Mestres, J., Gregori-Puigjané, E., Valverde, S. and Solé, R. V. (2009) The topology of drug-target interaction networks: implicit dependence on drug properties and target families. Mol Biosyst. 5, 1051-1057. https://doi.org/10.1039/b905821b), as any systems biologist will tell you, not least because folk differ massively (Williams, R. J. (1956) Biochemical Individuality. John Wiley, New York). This was and is well known in TCM etc. IMHO the failure to understand the role of transporters in drug disposition is also a major part of this (not enough = lack of efficacy; too much = tox, as per above). Latest version of that story at Kell, D. B. (2021) The transporter-mediated cellular uptake and efflux of pharmaceutical drugs and biotechnology products: how and why phospholipid bilayer transport is negligible in real biomembranes. Molecules. 26, 5629. https://doi.org/10.3390/molecules26185629.

I think the pivot that AI helps enable is programmable, scalable personalized therapies for cancer, PD, etc. Regulatory innovation will be critical because we’re not simply selling one-size-fits-all drugs, where regulators are taking a statistical analysis of the overall risk v. benefit for all comers. Algorithmic medicine - or digital biology - is the patient as their own control, or highly selected genotype/phenotypic cohorts. Small agile biotechs can go lightning fast in these types of settings…if we can get the manufacturing up to speed quickly enough.